What is SWIFT in Banking? Complete Guide to Global Payments & Messaging

What is SWIFT & How does It Work?

SWIFT payment System explained in simple words in this video.

Every day, trillions of dollars move across borders through an invisible but critical system. If you’ve ever wondered what is SWIFT in banking, you’re asking the right question. SWIFT is the backbone of international finance, yet most people misunderstand what it actually does.

What is SWIFT in banking? In simple terms, SWIFT is a secure global messaging network that banks and financial institutions use to exchange standardized instructions for cross-border payments and securities transactions. It does not move money itself. Instead, it carries the precise messages that tell banks exactly what to do with funds.

Table of Contents

- What is SWIFT in Banking? (Definition & What It Is NOT)

- The History of SWIFT

- How Does the SWIFT Network Work?

- Key Benefits of SWIFT for International Transfers

- SWIFT Transfer Fees and Hidden Costs (2026 Update)

- The Future of SWIFT in 2026: ISO 20022, Blockchain & Innovation

- Common Myths About SWIFT Debunked

- Conclusion: Why Understanding SWIFT Still Matters in 2026

What is SWIFT in Banking? (Definition & What It Is NOT)

SWIFT stands for Society for Worldwide Interbank Financial Telecommunication. Founded in 1973 and headquartered in Belgium, it operates as a member-owned cooperative serving more than 11,000 financial institutions across 200+ countries and territories.

Key clarification: SWIFT is a messaging network, not a bank or payment processor. It never holds funds, issues accounts, or settles transactions. Think of it as the highly secure “email system” of global finance, it delivers the instructions, while actual money moves through correspondent bank accounts or clearing systems.

Without SWIFT, international wire transfers would be slow, error-prone, and extremely expensive, like the old Telex system it replaced.

The History of SWIFT

Before SWIFT, banks relied on the outdated Telex network, slow, insecure, and lacking standardization. In 1973, seven major banks created SWIFT to solve this problem.

- 1977: SWIFT goes live with its first messages.

- 1980s–1990s: Rapid global adoption as international trade explodes.

- Today: SWIFT processes an average of over 40 million messages per day, making it the undisputed standard for high-value cross-border communication.

The system has evolved continuously, but its core mission remains the same: delivering secure, reliable, and standardized financial messaging worldwide.

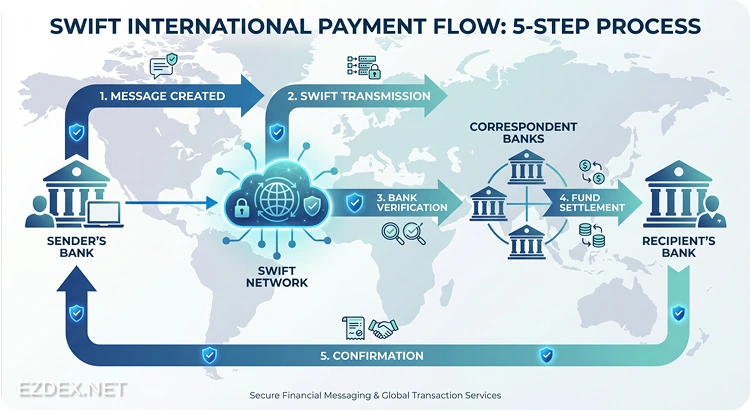

How Does the SWIFT Network Work?

Understanding the process helps demystify international payments. Here’s exactly how a typical SWIFT transfer flows:

Initiation: You instruct your bank to send money abroad. Your bank creates a standardized SWIFT message (usually MT103 for customer transfers).

- Transmission: The message travels securely through the SWIFT network to the recipient’s bank (or intermediary correspondent banks).

- Verification: Each bank validates the message format, checks compliance (AML/KYC), and confirms details.

- Settlement: Actual funds move via correspondent accounts or local clearing systems (this part is separate from SWIFT messaging).

- Confirmation: Final status messages are exchanged, and both parties receive confirmation.

Important note: The entire messaging process usually takes minutes, but the full transfer (including settlement) can take 1–5 business days depending on time zones, holidays, and intermediary banks.

Key Benefits of SWIFT for International Transfers

SWIFT remains the gold standard for high-value cross-border payments because of several undeniable advantages:

- Unmatched Global Reach: Connects over 11,000 financial institutions in more than 200 countries and territories. Whether you’re sending money to Tokyo, Lagos, or São Paulo, SWIFT can route the message.

- Military-Grade Security: Every message is encrypted and authenticated. SWIFT’s network is one of the most secure communication systems in the world, with multiple layers of monitoring and fraud detection.

- Standardization & Reduced Errors: All messages follow strict formats (MT and now ISO 20022). This dramatically lowers the risk of miscommunication that was common with older systems like Telex.

- Legal & Regulatory Compliance: Banks worldwide trust SWIFT because it helps them meet strict anti-money laundering (AML) and know-your-customer (KYC) requirements.

- Proven Reliability: For over 50 years, SWIFT has delivered consistent performance even during geopolitical crises and market turbulence.

For businesses and high-net-worth individuals handling large international transactions, these benefits often outweigh the slightly higher cost compared to newer alternatives.

SWIFT Transfer Fees and Hidden Costs (2026 Update)

One of the most common questions is: How much does a SWIFT transfer cost?

Typical fee structure in 2026:

- Sending bank fee: $15 – $50 (sometimes flat, sometimes percentage-based)

- Intermediary (correspondent) bank fees: $10 – $30 per bank (often 1–3 banks involved)

- Receiving bank fee: $10 – $25

- Foreign exchange (FX) markup: 1% – 4% above mid-market rate (this is often the biggest hidden cost)

Real example: Sending $10,000 USD to Europe can easily cost $45–$120 in total fees plus poor exchange rates. Always ask your bank for the full cost disclosure before confirming the transfer.

Pro tip: Compare the total cost (fees + exchange rate) rather than just the advertised SWIFT fee.

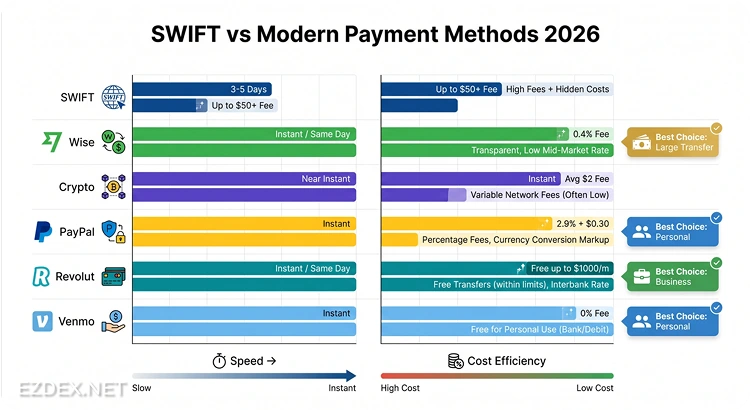

SWIFT vs Other Payment Methods (2026 Comparison)

Here’s a clear side-by-side comparison to help you choose the best option:

| Payment Method | Speed | Total Cost | Security Level | Best For | Limits |

| SWIFT | 1–5 business days | Medium–High | Very High | Large international transfers | High minimums |

| Traditional Wire | 1–3 business days | High | High | Domestic + some international | Bank-dependent |

| Wise / Remitly | Minutes–1 day | Very Low | High | Personal & SME transfers | Lower limits |

| PayPal / Venmo | Instant | Medium–High | High | Small personal payments | High fees for business |

| Cryptocurrency | 10–60 minutes | Very Low–Medium | Variable | Fast global value transfer | Volatility & regulation |

| Stablecoins (USDT) | Minutes | Very Low | High (on-chain) | Crypto-to-fiat & fast settlements | Requires exchange |

Key takeaway: SWIFT excels when you need maximum security and regulatory compliance for large sums. For smaller or time-sensitive transfers, modern fintech solutions often win on speed and cost.

The Future of SWIFT in 2026: ISO 20022, Blockchain & Innovation

The global payments landscape is undergoing its biggest transformation in decades. Here’s what’s happening right now:

ISO 20022 Migration (The Biggest Change Since 1973)

In November 2025, SWIFT retired most legacy MT message formats. From 2026 onward, ISO 20022 becomes the mandatory standard for all core payment messages.

Why it matters:

- Much richer, structured data (better compliance and fraud detection)

- Improved straight-through processing rates

- Enhanced tracking and transparency for regulators

- Foundation for real-time and 24/7 payments

Banks that haven’t upgraded yet are facing higher fees and processing delays in 2026.

SWIFT’s Blockchain & Shared Ledger Initiative

SWIFT is no longer just a messaging network. In 2025–2026 it launched a shared ledger platform built on blockchain technology (Hyperledger Besu). This allows tokenized deposits and atomic settlement between banks, dramatically reducing settlement risk and enabling true 24/7 cross-border payments.

These innovations position SWIFT to remain relevant even as cryptocurrencies and stablecoins gain traction.

Common Myths About SWIFT Debunked

Myth 1: “SWIFT actually moves the money.” Fact: SWIFT only carries instructions. The actual funds move through correspondent bank accounts or local clearing systems.

Myth 2: “SWIFT is outdated and will be replaced by crypto.” Fact: SWIFT is evolving faster than ever with ISO 20022 and its own blockchain ledger. It will coexist with, and even integrate, new technologies.

Myth 3: “Only big international banks use SWIFT.” Fact: Over 11,000 institutions use it, including central banks, corporates, securities firms, and many mid-sized banks.

Myth 4: “All international transfers use SWIFT.” Fact: Many domestic or regional payments use local systems (ACH, SEPA, FPS). SWIFT is mainly for cross-border high-value transactions.

Conclusion: Why Understanding SWIFT Still Matters in 2026

Whether you’re a business owner, freelancer, or investor moving money internationally, SWIFT in banking remains the most trusted and widely used system for secure cross-border communication.

The key takeaway is simple: SWIFT doesn’t move your money, it moves the information that makes the movement possible, safely and reliably.

As ISO 20022 and blockchain upgrades roll out throughout 2026, the system is becoming faster, more transparent, and more powerful than ever before.

Ready to make smarter international transfers? At EzDex we combine the reliability of traditional finance infrastructure with the speed of cryptocurrency. Explore our crypto-to-fiat services or read our other guides on BIC codes, transfer times, and the future of global payments.

Read the latest news and announcements in this section.

Read the latest tutorials about payment service providers in this section.

You can access full guides and tutorial to use EZDEX services in this section.

Step by step tutorials and photo guides are available in this section.

Access the latest information about financial and economical matters in Turkey in this section.

Explore expert guides, tips, and strategies for understanding and working with gold. Learn everything from basics to advanced knowledge.

Access the latest information about financial and economical matters in UAE in this section.

Expert articles and guides about silver, covering everything from fundamental concepts to advanced insights on investing and understanding the silver market.