Turkish Bank Interest Rates in 2026: Current Rates & How to Calculate Deposit Profits

In recent years, bank interest rates in Turkey have become one of the most attractive investment opportunities for foreign investors. Due to high inflation and the monetary policy of the Central Bank of Turkey, Turkish banks have offered unusually high deposit rates, often exceeding 30–40% annually.

These high rates have drawn the attention of many foreign investors, particularly from countries with unstable currencies, who are looking for ways to protect the value of their capital or generate high short-term returns.

However, with the start of 2026, economic conditions in Turkey are gradually changing. Interest rates are expected to decline as the central bank continues its efforts to stabilize inflation and strengthen economic policy.

In this article, we will explore:

Table of Contents

- Forecast for Turkish Bank Interest Rates in 2026

- Comparison of Popular Turkish Banks for Deposits

- Turkish Lira vs Dollar Deposits: Which Investment Is Better?

- A Common Strategy for Foreign Investors

- How Bank Interest Is Calculated in Turkey

- Taxes on Bank Interest in Turkey

- Online Turkish Bank Interest Calculators

- Is Investing in Turkish Bank Deposits Worth It in 2026?

- Conclusion

In December 2025, the Central Bank of the Republic of Turkey (CBRT) reduced its policy interest rate to 38%. This marked the fourth consecutive rate cut, signaling the beginning of a gradual monetary easing cycle.

The overnight deposit rate, which is the interest rate paid when banks deposit funds at the central bank for one day, declined to 36.5%.

Because commercial banks typically adjust their deposit rates based on the central bank’s policy rate, interest rates on Turkish lira savings accounts remain high but have begun to decline slightly.

Currently, the approximate deposit rates offered by Turkish banks are:

- Average 32-day short-term deposit: 35% – 43% annually

- State banks (such as Ziraat Bankası): around 31% – 39%

- Private banks (such as İş Bankası): around 34% – 35% for large deposits through mobile apps

- Some private banks (Garanti BBVA or QNB Finansbank): up to 43% through digital banking channels

Banks often offer higher rates for online deposits, meaning customers who open deposits through mobile banking or internet banking may receive better offers.

Smart savers don't just settle for standard rates! they strategically use Welcome offers to maximise their earnings, check out our Real-Time Comparison of Turkey’s Top Bank Welcome Rates to see which banks are leading the market

⚠️ Important: Interest rates for foreign currency deposits (USD or EUR) are extremely low, usually below 1% annually, which is common in most global banking systems.

Forecast for Turkish Bank Interest Rates in 2026

According to economic models and analyst forecasts, the Central Bank of Turkey will likely continue lowering interest rates gradually throughout 2026.

The main reason is the expected decline in inflation as tighter monetary policies implemented in previous years begin to take effect.

Economic projections from various financial research sources indicate:

- Policy interest rate: expected to fall to 25% – 28% by the end of 2026

- Average deposit rates: may decline to around 23% – 30%

- Inflation target: about 16% in the medium term

However, inflation forecasts vary widely depending on economic conditions. Some analysts estimate inflation may fall between 13% and 19%, while others believe it could remain higher, possibly reaching 22% or more.

If inflation drops faster than expected, the central bank may reduce interest rates more aggressively. On the other hand, if inflation remains persistent, higher interest rates could remain for longer.

Comparison of Popular Turkish Banks for Deposits

As of January 2026, Turkish banks still offer relatively high deposit rates compared with most countries.

Private banks usually offer more competitive rates than state-owned banks, especially through digital channels designed to attract new customers.

Below is a simplified comparison of several popular banks among foreign investors.

| Bank | Estimated Annual Deposit Rate | Notes for Foreign Investors |

| Ziraat Bankası | 31% – 39% | State-owned bank, relatively easier account opening |

| İş Bankası | 34% – 35% | Strong mobile banking system |

| VakıfBank | 39% – 40% | Competitive for larger deposits |

| Garanti BBVA | Up to 43% | Special online interest offers |

📌 Deposit rates change frequently depending on market conditions, deposit size, and promotions offered by banks.

Therefore, it is always recommended to check the latest rates directly through bank websites or mobile applications.

Turkish Lira vs Dollar Deposits: Which Investment Is Better?

One of the most important decisions for foreign investors in Turkey is choosing between:

- Turkish lira deposits

- Foreign currency deposits (USD or EUR)

Turkish Lira Deposits

Deposits in Turkish lira offer very high nominal interest rates, often between 35% and 40% annually.

These deposits can generate strong short-term profits, especially when:

- Inflation decreases

- Exchange rates remain relatively stable

However, the biggest risk is the devaluation of the Turkish lira.

Economic forecasts suggest that the Turkish lira may depreciate by another 10%–15% during 2026, potentially reaching around 48–50 lira per US dollar.

If the currency weakens significantly, it may reduce or even eliminate the profit from high interest rates.

Dollar or Euro Deposits

Deposits in USD or EUR are much safer from a currency perspective.

Advantages include:

- Capital value remains stable

- No exchange-rate risk

However, the downside is the very low interest rate, typically 0.5%–1% annually.

A Common Strategy for Foreign Investors

Many investors choose a mixed strategy:

Deposit part of their capital in Turkish lira to benefit from high interest rates.

Hold the rest in US dollars or euros to protect against currency fluctuations.

This strategy helps balance potential profits and currency risk.

How Bank Interest Is Calculated in Turkey

Turkish banks calculate deposit interest on a daily basis, using 365 days per year.

The standard formula used by banks is:

Interest = (Deposit Amount × Annual Interest Rate × Number of Days) ÷ 365

Example Calculation

Suppose you deposit:

1,000,000 Turkish lira

Annual interest rate: 35%

Deposit period: 30 days

The calculation would be:

Interest = (1,000,000 × 0.35 × 30) ÷ 365

Result:

28,767 Turkish lira profit for 30 days

If the same deposit is kept for one full year, the expected profit would be approximately:

350,000 lira before taxes

Taxes on Bank Interest in Turkey

Interest income from bank deposits in Turkey is subject to withholding tax.

Current tax rates are:

- Deposits up to 6 months: 15% tax

- Deposits between 6 and 12 months: 12% tax

- Deposits longer than 1 year: 10% tax

The tax is usually deducted automatically by the bank, so investors receive their net profit directly.

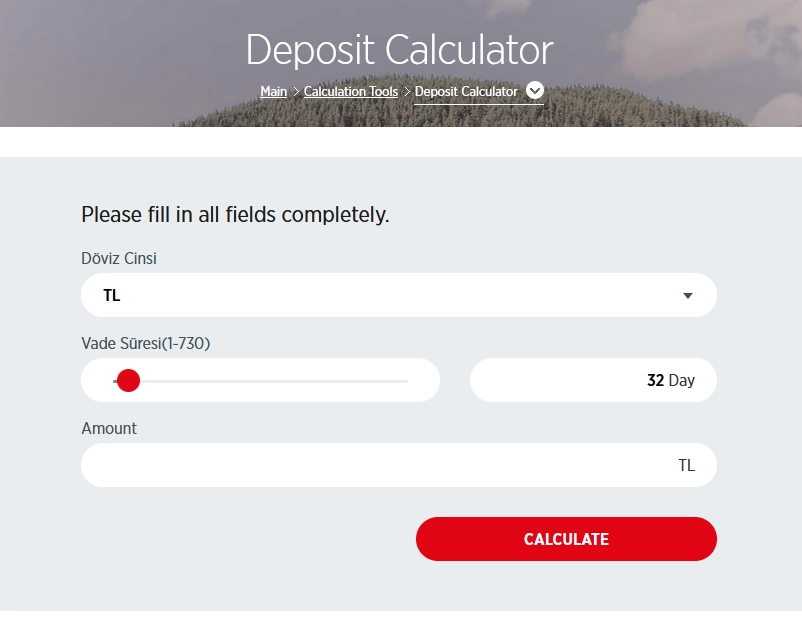

Online Turkish Bank Interest Calculators

Many Turkish banks provide online deposit calculators to estimate profits.

These tools allow users to calculate expected interest based on deposit amount, currency (TRY, USD, EUR), deposit duration and current interest rates.

Online calculators make it easy to compare potential returns before opening a deposit account in Turkey.

You can use the link below to calculate Ziraat bank inrerest online:

Is Investing in Turkish Bank Deposits Worth It in 2026?

For many investors, Turkish bank deposits remain attractive in 2026, especially for short-term investments.

However, several factors should be carefully considered:

- Inflation trends

- Central bank interest rate policies

- Turkish lira exchange rate volatility

- Tax rates on interest income

Since interest rates are expected to gradually decline, many experts recommend short-term renewable deposits rather than long-term commitments.

Conclusion

The year 2026 could be one of the last periods of extremely high bank interest rates in Turkey. As inflation stabilizes and monetary policy becomes more balanced, deposit rates are expected to gradually fall.

For investors considering Turkish bank deposits:

Short-term deposits may offer the best flexibility

Currency risk should always be monitored

Official sources such as central bank data and bank websites should be used for updated information

Before making any investment decisions, it is advisable to consult financial advisors or migration experts familiar with the Turkish banking system.

Read the latest news and announcements in this section.

Read the latest tutorials about payment service providers in this section.

You can access full guides and tutorial to use EZDEX services in this section.

Step by step tutorials and photo guides are available in this section.

Access the latest information about financial and economical matters in Turkey in this section.

Explore expert guides, tips, and strategies for understanding and working with gold. Learn everything from basics to advanced knowledge.

Access the latest information about financial and economical matters in UAE in this section.

Expert articles and guides about silver, covering everything from fundamental concepts to advanced insights on investing and understanding the silver market.

What is the current tl deposit interest rates turkey 2026?

EzDex: Hello. Most banks offer 40–46% gross for TL time deposits in 2026.